The GeoAI Revolution

Foundation models, generative satellite imagery, and agentic spatial reasoning are converging to create a $65B market.

- How Geospatial Intelligence Is Reshaping the Built World

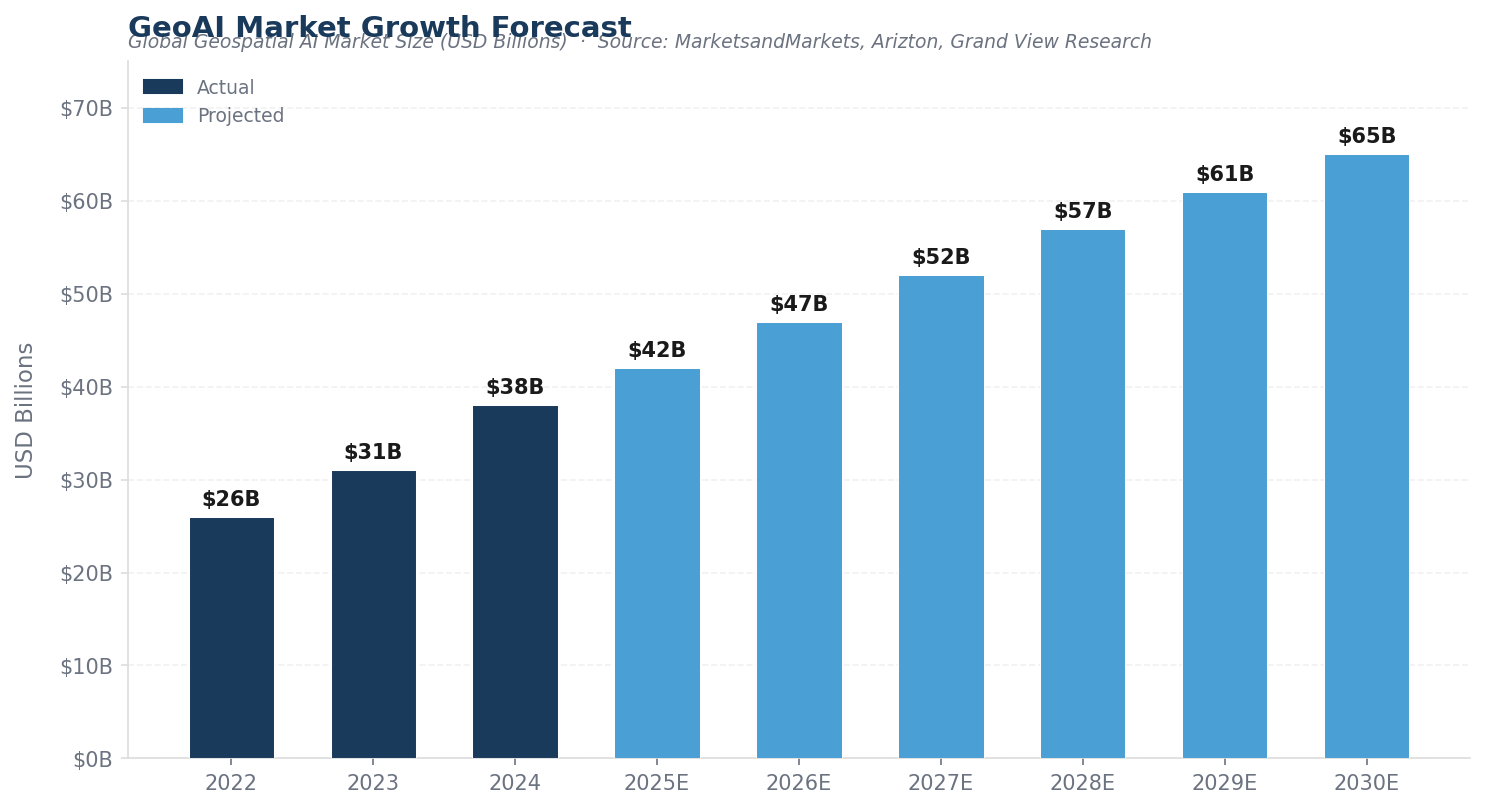

- GeoAI Market Size (2024)

- Projected by 2030

- 11.1%

Annual Space-Tech VC

Geospatial artificial intelligence is undergoing a paradigm shift. The convergence of foundation models, diffusion-based generative architectures, and large language models with Earth observation data is producing capabilities that were unimaginable just three years ago — and the implications for real estate, construction, and infrastructure are profound.

At MetaProp, we've tracked the collision of proptech and geospatial intelligence for over a decade. What we're witnessing now is different in both scale and kind: the pretrain-once, fine-tune-cheaply paradigm that transformed natural language processing is doing the same for satellite imagery, drone data, and spatial analytics. The result is a dramatic collapse in the cost and expertise barriers to planetary-scale environmental monitoring, urban planning, site assessment, and infrastructure management.

Three macro-trends are defining the landscape. First, the rise of geo-foundation models — massive neural networks pretrained on terabytes of unlabeled satellite imagery that can be fine-tuned for dozens of downstream tasks. Second, generative models that can synthesize, super-resolve, and temporally interpolate satellite imagery with unprecedented fidelity. Third, the integration of LLMs with geospatial reasoning to create agentic systems capable of answering complex spatial questions in natural language.

Together, these advances are creating an enormous opportunity for incumbents, startups, and investors alike.

- Market Trajectory

- GeoAI Market Growth Forecast

- Global Geospatial AI Market Size (USD Billions) · Source: MarketsandMarkets, Arizton, Grand View Research

The Technology Stack: From Pixels to Intelligence

The modern GeoAI stack has three distinct layers, each of which is being revolutionized simultaneously. At the foundation layer, models like NASA/IBM's Prithvi (pretrained on over 1TB of multispectral Landsat-Sentinel data) and ESA's TerraMind (integrating nine data modalities across 524 million Earth observation tiles) are proving that self-supervised pretraining works as powerfully for remote sensing as GPT proved for text.

At the generative layer, Stanford's DiffusionSat — the largest generative foundation model purpose-built for satellite imagery — is showing that diffusion architectures can synthesize cloud-free composites, predict future land-cover states, and upsample low-resolution imagery by over 20x. And at the reasoning layer, Stanford's GeoLLM research revealed that large language models encode surprising amounts of latent geospatial knowledge, opening the door to agentic systems that can query satellite archives and reason about spatial relationships in plain English.

For the built environment, these aren't academic curiosities. They translate directly into faster site assessment, automated change detection, real-time construction monitoring, predictive urban planning, and dramatically lower costs for infrastructure inspection.

Competitive Landscape

The GeoAI Competitive Landscape

Key players across the geospatial intelligence ecosystem — incumbents, startups, and investors driving the market forward

- Esri (ArcGIS)

- Google (Earth Engine)

- Trimble

- Hexagon AB

- Bentley Systems

- Planet Labs

- Maxar Technologies

- Autodesk

- IBM (Prithvi / NASA)

- Palantir Technologies

- Airbus Defence & Space

- AirWorks ★ MetaProp

- Orbital Insight

- BlackSky Technology

- Wherobots

- SatSure

- LiveEO

- AiDash

- Kayrros

- Capella Space

- Satellogic

- MetaProp ★ Proptech VC

- Sequoia Capital

- a16z

- In-Q-Tel

- Space Capital

- NGP Capital

- Seraphim Space

- PSG Equity

- Lux Capital

- March Capital

- Crosslink Capital

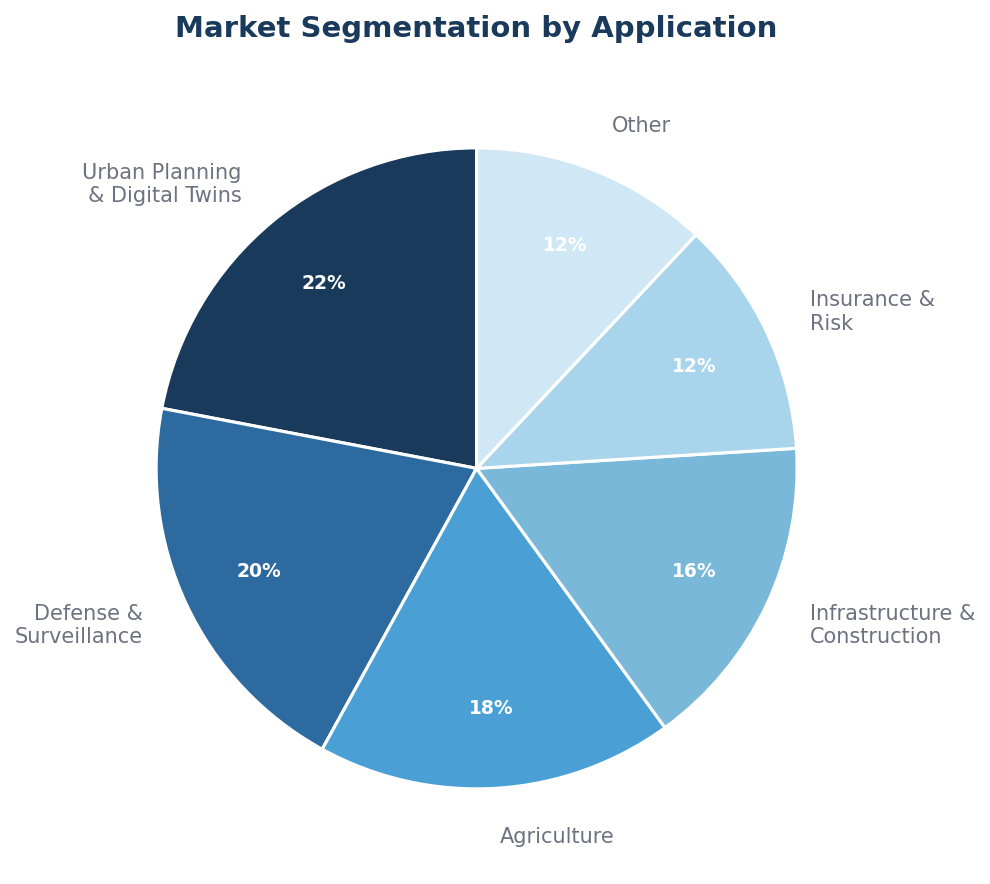

- Market Segmentation

- Fastest-growing verticals in GeoAI (% of market)

- Urban Planning & Digital Twins

- 22%

- 12.8% CAGR — fastest growing segment

- Defense & Surveillance

- 20%

- Persistent monitoring, data fusion

- Agriculture

- 18%

- Precision farming, crop health monitoring

- Infrastructure & Construction

- 16%

- Automated surveying, change detection

- Insurance & Risk Assessment

- 12%

- Claims validation, catastrophe modeling

- Other (Logistics, Energy, etc.)

- 12%

- Supply chain, grid monitoring

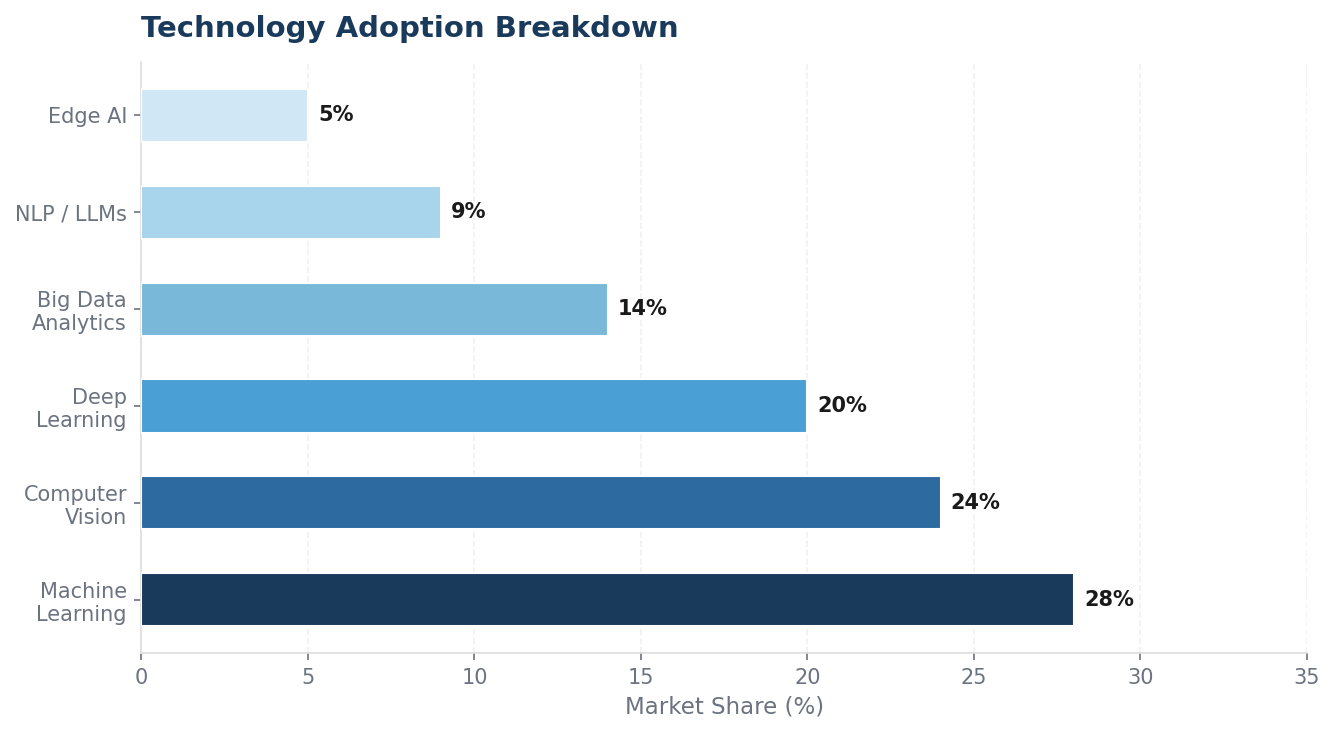

- Technology adoption breakdown in GeoAI solutions

- Machine Learning

- 28%

- Classification, prediction, pattern recognition

- Computer Vision

- 24%

- Feature extraction, object detection, change detection

- Deep Learning

- 20%

- Foundation models, semantic segmentation

- Big Data Analytics

- 14%

- Processing massive EO datasets at scale

- NLP / LLMs

- 9%

- Agentic spatial reasoning, GeoLLM

- Edge AI

- 5%

- Real-time drone & autonomous processing

The Proptech Angle: Why This Matters for the Built Environment

The real estate and construction industries have historically been among the slowest to adopt new technology. But geospatial AI is different — it addresses pain points that are too acute to ignore. Labor shortages have left AEC firms scrambling to hire. Projects are becoming more complex with increasingly compressed schedules. And the data bottleneck between field capture and actionable deliverables remains one of the industry's most persistent inefficiencies.

This is precisely where the proptech opportunity lives. Urban planning and digital twins represent the fastest-growing application segment in the geospatial intelligence market, projected to grow at a 12.8% CAGR through 2030. Insurance risk assessment and claims validation — powered by satellite and drone imagery analysis — is experiencing explosive demand. And construction monitoring, site selection, and environmental compliance are all being transformed by AI-powered spatial analytics.

Portfolio Spotlight

AirWorks: GeoAI for the Built World

MetaProp portfolio company AirWorks exemplifies how geospatial AI is being applied to solve real infrastructure challenges today. Spun out of MIT in 2018, AirWorks uses AI-powered computer vision to transform raw aerial data — from drones, LiDAR, satellite imagery, and orthomosaics — into survey-grade CAD and GIS deliverables in a fraction of the time traditional methods require.

The company serves telecommunications, power, and civil engineering firms, turning weeks of manual drafting into days of automated feature extraction. With over 100 standardized layers and patented pixel-based algorithms, AirWorks has established itself as the leader in automated mapping, deployed with some of the largest civil engineering and telecom companies worldwide.

Customers have reported 70–80% reductions in drafting time, significant cost savings over additional manpower, and the ability to deliver more projects faster — exactly the kind of ROI that makes geospatial AI adoption a no-brainer for infrastructure firms.

- Total Funding

- 100+

- Customers

- 70–80%

- Time Reduction

- Spinout Origin

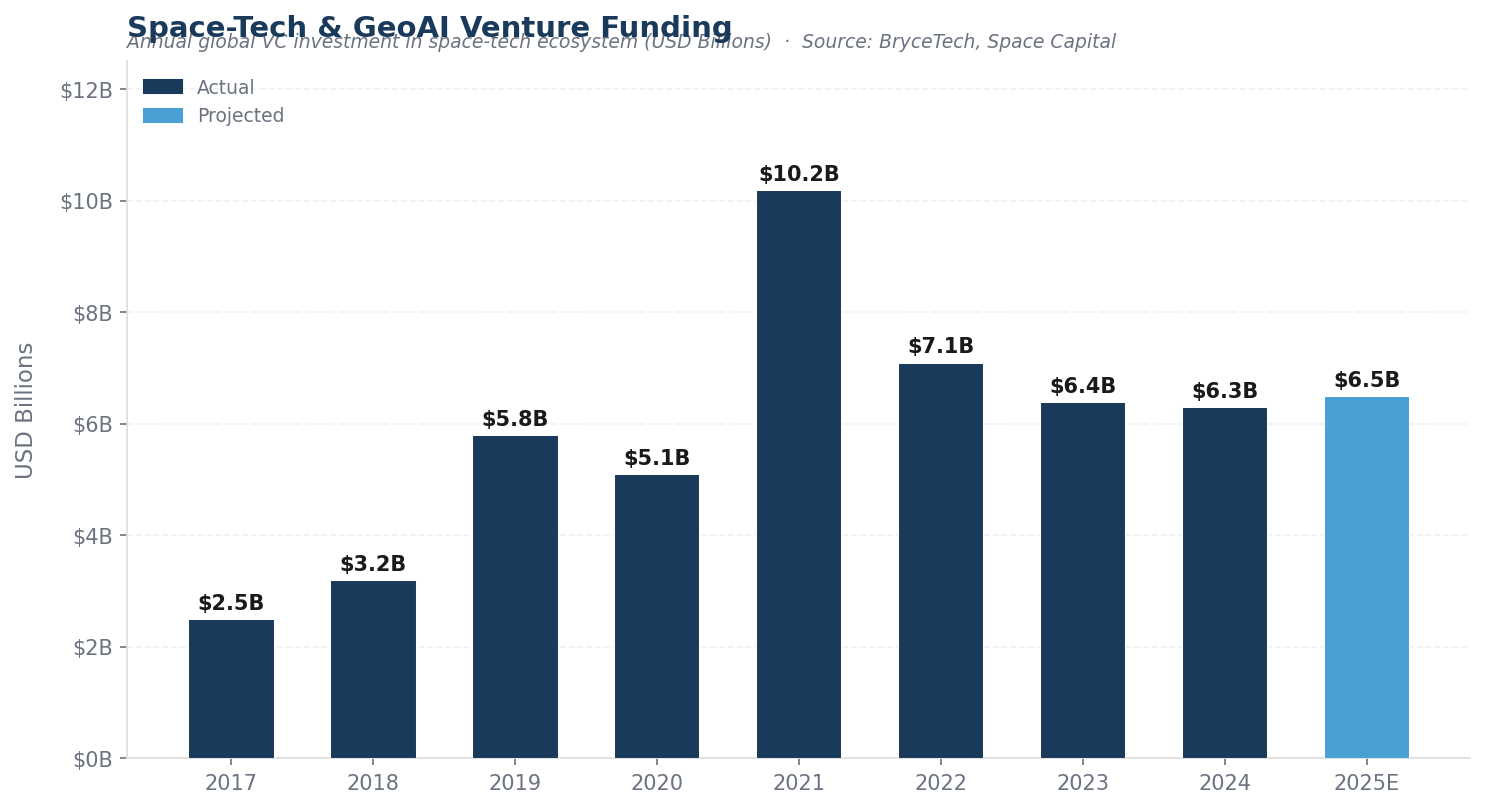

- Venture Landscape

- Space-Tech & GeoAI Venture Funding

- Annual global VC investment in space-tech ecosystem (USD Billions) · Source: BryceTech, Space Capital

The Research Driving It All

The commercial GeoAI boom is being powered by an extraordinary wave of academic research. Stanford's Ermon Group has been particularly prolific, producing three landmark papers:

- SatMAE (NeurIPS 2022) — showed that self-supervised pretraining adapted for temporal and multi-spectral satellite data dramatically outperforms supervised baselines

- DiffusionSat (ICLR 2024) — adapted latent diffusion models for satellite imagery by conditioning on geospatial metadata

- GeoLLM (ICLR 2024) — demonstrated that LLMs prompted with geographic coordinates can yield accurate predictions of socioeconomic indicators and land use

MIT's Senseable City Lab is pioneering LiDAR-based urban mapping and 15-minute-city mobility analytics. Carnegie Mellon's collaboration with Fujitsu on Social Digital Twin technology is transforming 2D monocular camera feeds into real-time 3D urban scene reconstructions. And Columbia's Center for Spatial Research ensures the field grapples with fairness, privacy, and equitable access as these tools become more powerful.

At the infrastructure layer, NASA/IBM's Prithvi model proved that the foundation-model paradigm transfers powerfully to Earth observation, and its open-source release on Hugging Face has catalyzed an entire ecosystem. ESA's TerraMind, with its nine-modality integration across optical imagery, SAR, elevation models, weather data, and textual annotations, represents the most ambitious multi-modal EO foundation model to date.

- Our Thesis

- Five Themes Defining the GeoAI Opportunity

- 01

Foundation Models Collapse Costs

Geo-foundation models like Prithvi and TerraMind are reducing the cost of building operational remote-sensing pipelines from millions to thousands of dollars — democratizing access for startups and midmarket firms alike.

02

Generative AI Meets the Planet

Diffusion models can now generate, super-resolve, and temporally interpolate satellite imagery. This unlocks synthetic training data, cloud removal, and predictive land-cover modeling at scale.

03

LLMs as Spatial Reasoners

Language models encode latent geographic knowledge. The next frontier is agentic systems that call geospatial tools, query satellite archives, and reason about spatial relationships in natural language.

04

Digital Twins Go Mainstream

Real-time 3D reconstructions of urban environments — from cameras, LiDAR, and mobility data — are delivering situational awareness for traffic, disaster response, construction monitoring, and planning.

05

Proptech at the Epicenter

Real estate, construction, and infrastructure represent the highest-value application layer for geospatial AI. Site selection, automated surveying, risk assessment, construction monitoring, and smart city planning all sit at the intersection of spatial intelligence and the built environment — and startups like AirWorks are proving the model works today.

What We're Watching

The GeoAI market is evolving fast. Space-tech venture funding has held steady above $6 billion annually, with investors increasingly focused on the AI-powered analytics layer rather than hardware and launch. Planet Labs' recent partnership with Anthropic to use Claude for geospatial data analysis signals the mainstreaming of LLM-powered spatial intelligence. And the rise of vertical geospatial intelligence startups — companies like AirWorks, LiveEO, AiDash, and Kayrros that combine unique datasets with deep learning to solve specific industrial use cases — represents a massive opportunity for the venture ecosystem.

For real estate and construction, the message is clear: geospatial AI is no longer a niche tool for defense and government. It's becoming foundational infrastructure for how we plan, build, and manage the physical world. The startups that figure out how to package these capabilities into workflows that AEC professionals actually use — turning weeks of fieldwork into days, transforming raw data into actionable intelligence, and making spatial analytics as accessible as a search bar — will capture enormous value.

At MetaProp, we're excited to be backing founders at this intersection. The GeoAI revolution is here, and it's being built on top of the most ambitious research in the history of Earth observation.

Disclaimer: This blog post is for informational purposes only and does not constitute investment advice. AirWorks is a MetaProp portfolio company. Market data sourced from MarketsandMarkets, Arizton, Grand View Research, BryceTech, and Space Capital. Research citations refer to publicly available academic papers.