Our View Heading into Global Alts in Miami

From vertical AI in real assets, insurance, fintech, and infrastructure to shifting capital allocator dynamics, here's what's on our mind heading into Global Alts 2026.

- Inside the ideas shaping

- tomorrow's built world

- The MetaProp Blog offers in-depth perspectives on the technologies transforming how we finance, insure,

- design, manage, measure, build, and power the world.

- heading into Global Alts 2026.

- Charlotte Glatt

Head of Capital Formation, MetaProp

Next week, the MetaProp team will be in Miami for iConnections Global Alts 2026 — the world's largest capital introduction event — joining over

5,000 attendees, 1,200 institutional allocators, and 850 fund managers for four days of panels, one-on-one meetings, and the kind of candid corridor

conversations that actually move capital.

We're looking forward to reconnecting with limited partners, fellow GPs, and the broader alternatives community. The team is coming to Miami with

a clear point of view. It's been shaped by more than a decade and 175+ investments at the intersection of technology and the built world, and

sharpened by two years of watching generative AI reshape investing in real time. Here's what's on our mind heading into the week.

The Vertical AI Opportunity

The AI investment conversation has matured considerably since the foundation model hype cycle of 2023. Most institutional allocators we speak with

have moved past the question of whether AI matters. The harder question they're now wrestling with is: where in the stack does venture-scale value

accrue — and how do I get exposure without making a leveraged bet on a rapidly commoditizing infrastructure layer?

Our conviction — and the thesis we've been building toward since well before this cycle — is that the most durable, risk-adjusted returns in AI will

come from vertical AI companies. Purpose-built applications that embed deep domain expertise into regulated, data-rich industries where switching

costs are high and incumbents are slow to move. Industries like real estate. Insurance. Financial services. Energy infrastructure. Digital infrastructure.

These aren't the companies grabbing headlines for raising $500 million seed rounds to train the next frontier model. They're the companies quietly

signing seven-figure enterprise contracts with REITs, insurance carriers, mortgage originators, and utility operators — customers who care far less

about model architecture and far more about whether the product reduces their loss ratio, compresses their underwriting timeline, or automates the

40% of their back office that still runs on spreadsheets and phone calls.

At MetaProp, we've spent ten years building the pattern recognition to identify these vertical AI companies early. Our strategic LP base —

representing over 20 billion square feet of real assets across every property type and global market — gives our portfolio companies something no

metaprop | metaprop.com/blog | 214 W 39th St Suite 705, New York, NY 10018

horizontal AI fund can replicate: a built-in distribution channel and pilot-ready sandbox in the exact industries where AI is creating the most

measurable value.

New Allocator Dynamics in a New Era

In our conversations with pensions, endowments, family offices, and sovereign wealth funds, we hear a consistent set of tensions that define the

current moment:

Valuation discipline vs. deployment pressure. Everyone recognizes AI as transformative. But the memory of 2021 vintage markups — and the

subsequent write-downs — is fresh. Allocators are asking: how do I get meaningful AI exposure without overpaying at the infrastructure layer, where

competitive dynamics are most intense and margins are compressing? Our view is that the answer lies in the application layer, where companies solve

specific, measurable problems for specific, measurable customers. Vertical AI in real assets, insurance, and financial services is where valuations

remain rational and enterprise willingness-to-pay is already proven.

Diligence complexity. Evaluating AI-native companies requires a different underwriting muscle than evaluating traditional SaaS. How defensible is

the data moat when foundation models improve every quarter? Does the next generation of models help or hurt the company's competitive position?

Is the AI actually doing something differentiated — or is this a thin wrapper over an API call? Our team evaluates these questions every week across

200+ new PropTech companies we screen monthly. We recognize they're meaningfully harder for generalist allocators to underwrite without deep

sector-specific expertise.

Portfolio construction ambiguity. Where does vertical AI for real assets and financial services fit within an institutional portfolio? Is it venture

capital? Real estate? Fintech? Infrastructure? The honest answer is that it touches all four, and the allocators moving fastest are the ones who've

stopped trying to force it into a single bucket. They're recognizing vertical AI as a thematic allocation that cuts across their existing book — one that

offers both technology upside and direct relevance to the physical-world assets they already own.

The M&A acceleration. Our latest Global PropTech Confidence Index found that 78% of investors now expect increased M&A activity — a record

high. Industry consolidation is accelerating as larger incumbents seek strategic acquisitions to expand AI capabilities and operational efficiencies. For

early-stage investors, this creates a dual-exit environment: strategic acquisitions and growth-stage financings are both active, compressing the time-

to-liquidity for category-leading vertical AI companies.

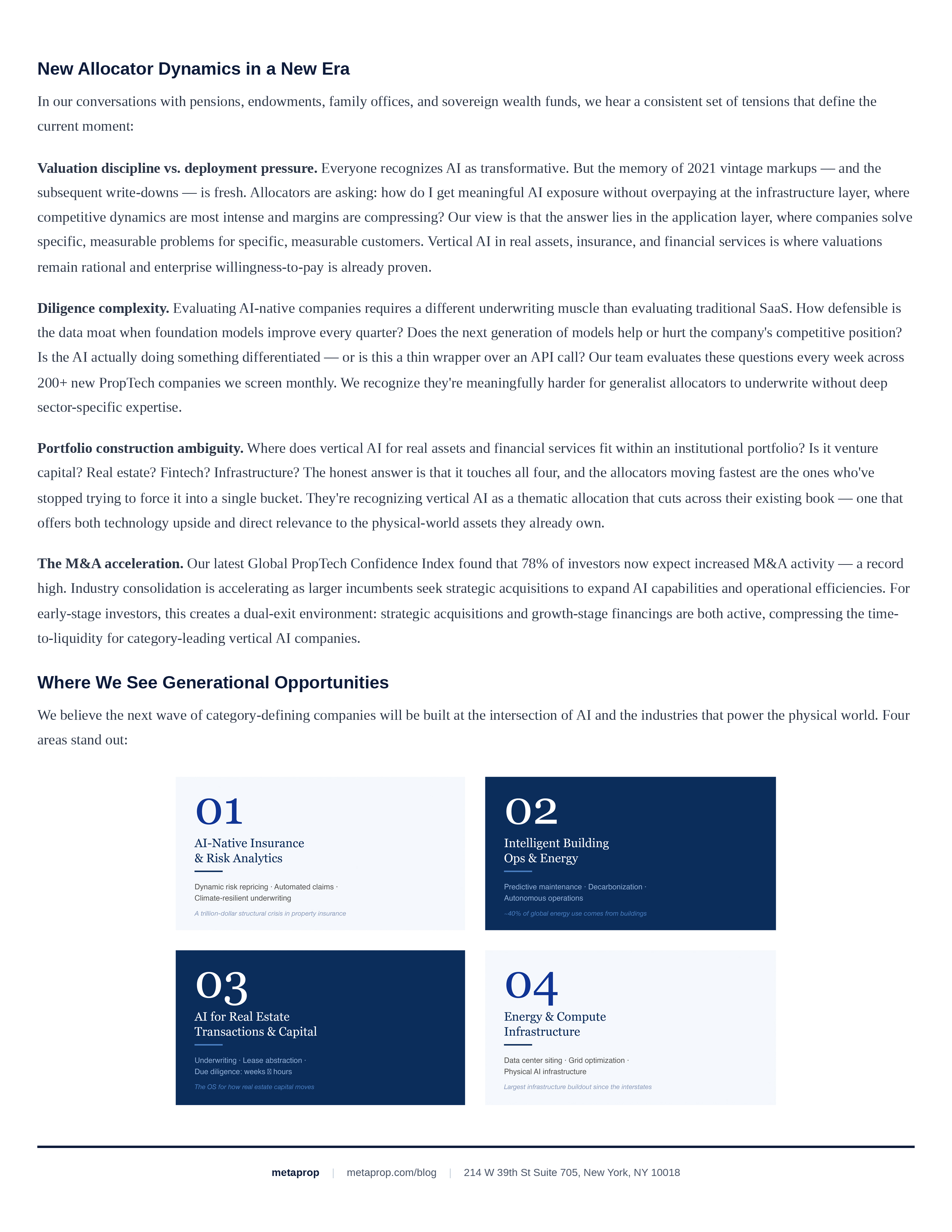

Where We See Generational Opportunities

We believe the next wave of category-defining companies will be built at the intersection of AI and the industries that power the physical world. Four

- areas stand out:

- metaprop | metaprop.com/blog | 214 W 39th St Suite 705, New York, NY 10018

AI-Native Insurance and Risk Analytics. The property insurance market is in structural crisis. Carriers are pulling out of entire states. Premiums are

spiking. And the underlying risk models were built for a climate that no longer exists. AI companies that can reprice risk dynamically, automate

claims adjudication, and give carriers the confidence to write policies in wildfire zones and flood plains are solving a trillion-dollar problem — one

that directly impacts every institutional portfolio with real asset exposure.

Intelligent Building Operations and Energy Transformation. Commercial buildings represent roughly 40% of global energy consumption.

Generative AI is enabling a step-change in how buildings are monitored, optimized, and decarbonized — moving from reactive maintenance to

predictive, autonomous operations. For every REIT, every pension fund with real asset holdings, and every corporation with a net-zero commitment,

this is no longer an innovation play. It's an operational imperative.

AI for Real Estate Transactions and Capital Markets. Underwriting, appraisal, lease abstraction, due diligence — these are workflows that have

historically required armies of analysts and weeks of manual effort. AI is compressing that timeline from weeks to hours. The companies leading this

compression aren't just building point solutions. They're building the operating system for how real estate capital moves — from origination through

disposition.

Energy and Compute Infrastructure. The AI revolution requires a physical backbone. The demand surge for data center capacity, power

infrastructure, and edge computing sits squarely within the real assets ecosystem and represents one of the largest infrastructure buildouts since the

interstate highway system. A new class of vertical AI companies is emerging to site, develop, power, and manage the physical layer of the AI

economy. PropTech and digital infrastructure are converging — and the investment implications are enormous.

Why Now

iConnections Global Alts brings together the right audience at the right moment: allocators actively deploying capital, sophisticated enough to see

past the noise, and searching for managers with genuine domain conviction in the sectors where AI creates the most lasting value.

Over $16.7 billion in venture and private-credit capital flowed into real estate, construction, and infrastructure technology in 2025 alone. This isn't

speculative — it's institutional. And the allocators who move early into vertical AI exposure within these sectors will be best positioned as the

convergence of real assets, financial services, and AI deepens over the coming decade.

If you're at Global Alts this week, we'd love to connect. Whether you're assessing how vertical AI fits into your portfolio, building at the intersection

of AI and the built world, or investing through the same lens — let's talk.

metaprop | metaprop.com/blog | 214 W 39th St Suite 705, New York, NY 10018