Navigating the Property Insurance Crisis

How dramatic insurance premium increases have made certain housing markets fundamentally unaffordable and what AI and data can do to help.

A Practical Playbook: Navigating the Property Insurance Crisis

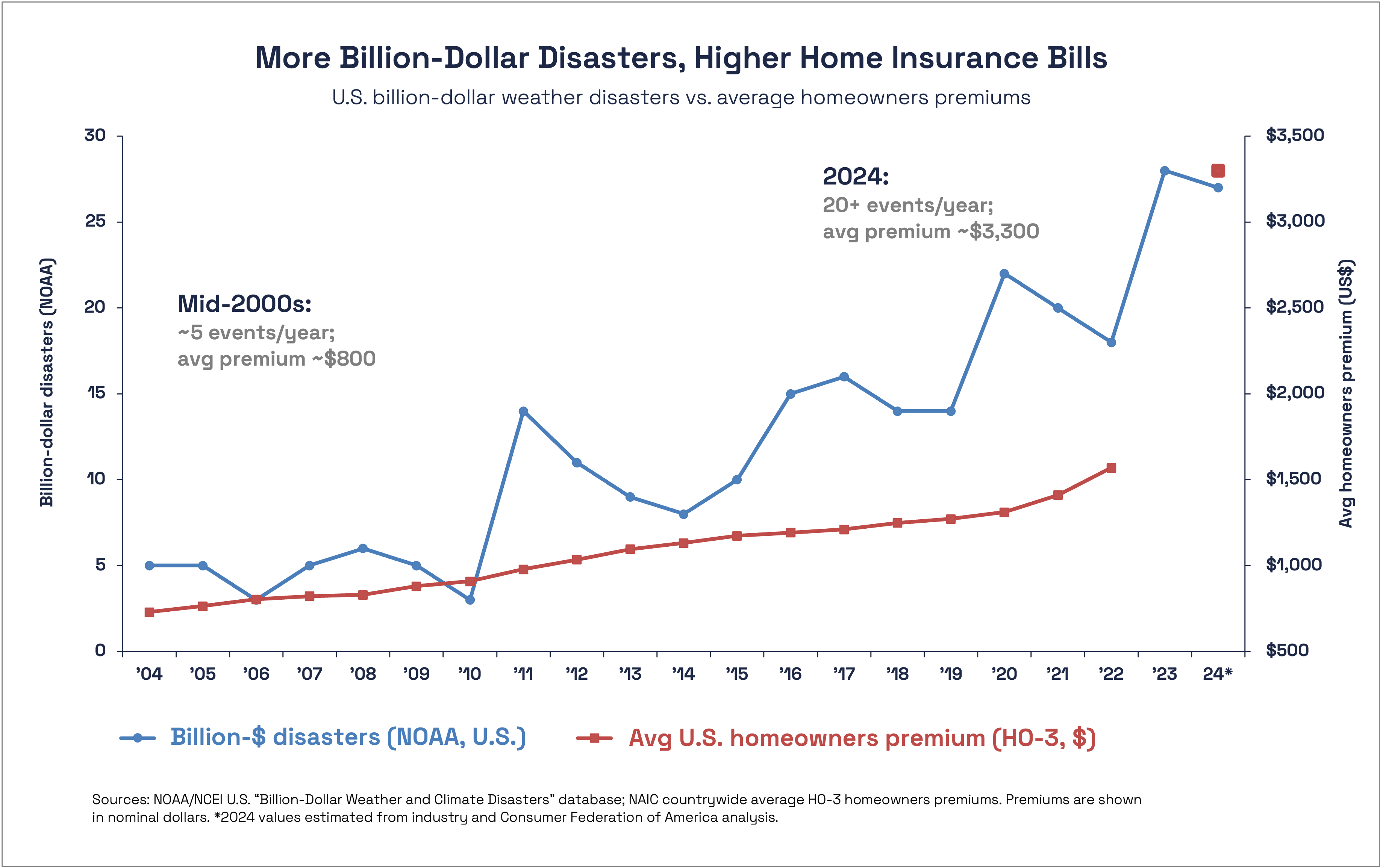

Property insurance is becoming a line item that can make—or break—homeownership and operating budgets. Premiums surged across the U.S. again last year as climate-amplified disasters drove higher losses and reinsurers passed through more cost. In 2022 alone, average U.S. homeowners premiums jumped 11.2% (the fastest pace in a decade); from 2018–2022 they rose 8.7% per policy, after inflation. And by 2024, consumer analysts estimated a ~24% three-year climb, with “typical” annual premiums breaching $3,300 (methodologies differ, but the trend is unambiguous). (S&P Global, Fortune)

Behind those increases: a drumbeat of record disasters. NOAA counted 27 separate U.S. weather and climate events topping $1B each in 2024—just shy of the all-time record—while Swiss Re tallied $137B in global insured catastrophe losses in 2024 and says the long-run trend is still rising 5–7% annually in real terms. (NCEI, Swiss Re)

The human impact is real. In many markets, taxes and insurance now consume a historically large slice of the monthly housing payment; insurers, meanwhile, have pulled back or non-renewed in high-risk states, forcing households onto last-resort plans or going bare. California regulators have even green-lit new rules that will likely raise rates (by passing through reinsurance costs and enabling wildfire catastrophe models) in exchange for improved availability in fire-prone areas. That’s a painful tradeoff—pay more, but at least get coverage. (ReinsuranceNe.ws, CAPE Analytics, AP News)

Good news: real estate and insurance technology can’t change the weather (yet), but can change the math. Below is a practical playbook—tools you can deploy over the next 12–24 months to slow premium growth, win credits, and make your assets more insurable.

1) Get radically better risk data (pricing power starts with precision)

Public platforms

- Verisk (NYSE: VRSK) – catastrophe models and property analytics (Extreme Event Solutions) used to price wind, flood, wildfire and more; widely embedded in underwriting and claims workflows.

- Moody’s RMS (NYSE: MCO) – risk models and climate analytics used by carriers and reinsurers to price and manage cat exposure. (Fintech Global)

- Guidewire (NYSE: GWRE) – core P&C systems; acquired HazardHub, a geospatial data provider with 950+ risk variables (air, water, earth, fire) that prefill property risk in underwriting. (SEC)

- Sapiens (NASDAQ: SPNS) – P&C core platforms that digitize rating/underwriting to reduce expense and error rates. (Insurance Industry Blog)

Early-stage & growth companies

- ZestyAI (Z-FIRE™) – AI wildfire risk at the property level; approved and used in rate/underwriting filings in multiple western states (including California). Recent post-event validations show strong alignment with 2025 SoCal fire footprints. (ZestyAI, ReinsuranceNe.ws)

- CAPE Analytics – computer-vision roof and property condition data from aerial imagery to cut inspections and improve selection. (The MortgagePoint -)

- Betterview (MetaProp portfolio company) – roof & property intelligence integrated with carrier workflows (now part of Nearmap’s aerial imagery stack). (Scotsman Guide)

- Arturo – property analytics used to prefill attributes and reduce time-to-quote. (mymortgagemindset.com)

- Delos Insurance (MGA) – uses wildfire science and satellite imagery to write homes many standard carriers won’t touch; an example of data unlocking supply where the market has retreated. (PR Newswire, iireporter.com)

- Faura (MetaProp portfolio company) - works with homeowners and insurance companies to help insurance carriers obtain better data on the resiliency of their homes, while guiding the homeowner on how to make their home more resistant to flood, fire and other natural disasters in order to obtain a more affordable insurance policy.

Why it matters: More granular, explainable risk data allows carriers to segment fairly (reward mitigation instead of blanket surcharges) and helps owners prove resilience—key to unlocking credits and avoiding blunt non-renewals.

- 2) Prevent the loss (instrument your buildings)

- Insurers increasingly reward verified risk-reduction. Two categories consistently pay back:

- Electrical fire prevention: Ting (Whisker Labs) monitors electrical arcing—the #1 cause of home fires—and dispatches licensed electricians when hazards are detected. State Farm provides Ting to many policyholders and runs a safety program around it. Fewer fires = fewer cat-adjacent claims. (arbol.io, FloodFlash)

- Water-leak mitigation: Whole-home and point-of-use leak sensors/valves (e.g., Flo by Moen, Phyn; commercial: WINT) cut non-weather water losses and can earn discounts or favorable terms with certain carriers and lenders. (Zillow)

Play it with purpose: Start where loss dollars are biggest in your portfolio (older electric panels, flat roofs, vacation/short-stay units, student housing). Instrument, document, and share the data with your broker/carrier during renewal to justify credits.

3) Harden the structure (and get credits for it)

The IBHS FORTIFIED standards (especially FORTIFIED Roof) codify construction practices that improve wind and water performance; after major wind events these homes systematically fare better than code-minimum peers. Several states require premium discounts for FORTIFIED features (e.g., Oklahoma statute). Some public grant programs help fund upgrades (e.g., Alabama’s Strengthen Alabama Homes).

Owner checklist: next time a roof is due, upgrade to a FORTIFIED roof assembly; add secondary water barriers, ring-shank fasteners, and enhanced edge details. Pair this with defensible-space landscaping and ember-resistant vents in wildfire zones—then ask your carrier to rate to the actual risk, not the ZIP code.

4) Modernize carrier and broker ops (expense ratio ≈ premium pressure)

Operational drag shows up in your rates. Carriers that replace legacy stacks with Guidewire/Sapiens and integrate property prefill, straight-through underwriting, and automated claims can lower expense and loss-adjustment costs (LAE), which feeds into pricing. On the claims side, companies like Lemonade and Obie (a MetaProp portfolio company) report AI triage/settlement that takes seconds in simple cases—illustrating how automation can compress cost while improving CX. (World Economic Forum, Q4 Capital, Lemonade)

Why owners care: markets with digitally efficient carriers tend to see less blanket pricing and faster endorsements—useful when you document mitigations mid-term.

5) Add parametrics and “gap-fillers”

Traditional indemnity policies struggle with speed and basis risk in perils like flood and hail. Parametric products pay a preset amount when a trigger (river stage, wind speed, local hail size) is met—often in days, not months. For example, FloodFlash offers sensor- or gauge-triggered flood coverage via brokers in the U.S., expanding options for small businesses and some residential exposures. The Demex Group (a MetaProp portfolio company) packages parametric hail/freeze programs that can sit alongside property policies. (Center for American Progress, firststreet.org)

Owner tactic: use parametrics to cover deductibles, business interruption, or markets where carriers limit sub-perils. The goal is a stacked program that caps tail risk without exploding total premium.

What real estate owners/operators can do this renewal cycle

- Map your exposure and forecast premiums. Pull parcel-level wildfire/wind/flood scores (from providers above) for each asset and roll to a portfolio view; share with brokers to steer the marketing narrative away from blunt averages. (thedemexgroup.com, Fintech Global)

- Install high-ROI sensors (Ting + water) at the riskiest assets first; collect work orders and event logs to document avoided losses. (FloodFlash)

- Upgrade the next roof to FORTIFIED and pursue state credits/grants where available; photograph and keep invoices for underwriting files. (getdelos.com)

- Negotiate for mitigation-based credits and higher sub-limits once proof is in hand; ask carriers to rate to property-level characteristics (roof age/material, defensible space, elevation, drainage). (SEC)

- Fill gaps with parametrics to cap deductibles/retentions in hail, flood, or wildfire smoke outages. (Center for American Progress)

The outlook—and why action beats waiting

Barring a policy sea-change, the industry will keep repricing toward physical risk as disasters remain elevated. NOAA’s five-year average now runs ~23 billion-dollar U.S. events a year, up from ~9 historically; reinsurer research suggests annual insured losses will keep climbing. Availability is improving in some states thanks to regulatory changes—but often at higher prices. That makes mitigation + measurement the most durable lever owners and communities control. (NCEI, Swiss Re, AP News)

- If you’re a developer, REIT, or HOA, the path to bending your insurance cost curve is clear:

- instrument the risk,

- harden the structure,

- prove it with data, and

- shop smarter products.

That won’t stop storms or fires. It will keep more homes and communities insurable—and keep more families from losing them to a line item they can no longer afford.